So, how can we avoid these latter-day financial sirens who lure us to shipwreck on their rocky

shores? First, we must recognise reality as it. Because, as Nobel physicist Richard Feynman said

after the Challenger space shuttle disaster:

“For a successful technology, reality must take precedence over public relations, for nature cannot be

fooled”.

Part 1 of this new series places the serial underperformance of European active funds under the

cold light of day. And we open the lid on the marketing tricks used to disguise this problem.

Part 2 will examine the murky world of fees.

Finally, Part 3 will share with you a framework we developed as a hedge fund, designed to make

your money works hard you, not everybody else.

Paying to Underperform: It’s more entrenched than you think

Every fund underperforms sometimes, we all know that. But the prevailing wisdom is that highly

paid active fund managers generally get it right longer term. Right?

Wrong! To see this, we must blow away the marketing fog and replace it with a reliable and

impartial scorekeeper. A role which, since 2002, has been dutifully fulfilled by S&P Dow Jones with

its provocatively named “S&P Indices versus Active Scorecards”, or “SPIVA Scorecards”.

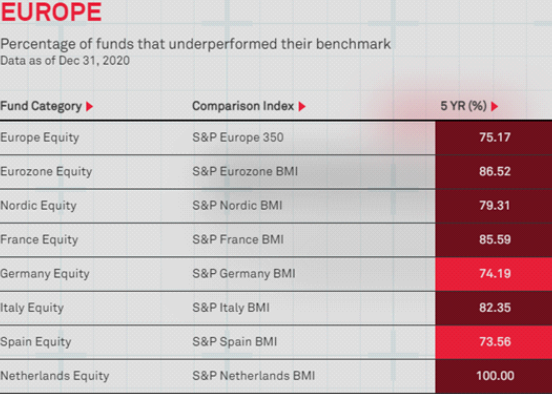

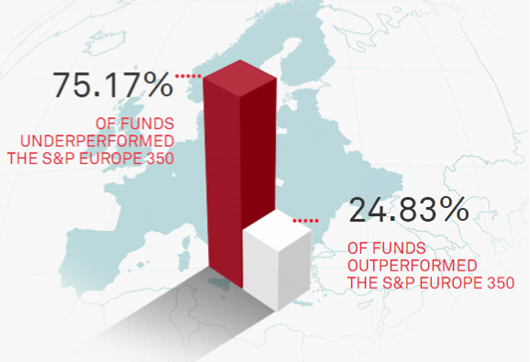

Right off the bat, SPIVA tells us that, over the past 5-years, a surprising 75% of European active

equity funds underperformed the benchmark S&P Europe 350 Index (Figure 1).

Over this same 5-year time horizon, 86% of active Eurozone-specialist funds underperformed

their relevant index, 85% of French-focussed funds underperformed, and as for specialists in

Dutch equities, not a single one outperformed (Figure 2).

Ouch!

Let’s go back still further to check we’re not missing anything. Over a 10-year time horizon,

the proportion of active European stock funds performing worse than their benchmark, increases

from 75% to 86%. And it keeps on increasing the further back in time we go.

A similar picture is visible in U.S., U.K., and Japan.

Do emerging market and other specialist funds fare better? Surprisingly not. According to

S&P Dow Jones, a hefty 96% of active emerging market funds underperformed their index over

the past 10-years, as did 98%, and 95% of Global Equity, and US Domestic specialist funds,

respectively.

Figure 1: Underperformance of Active European Stock Funds (5 Yrs)

https://www.spglobal.com/spdji/en/spiva/#/reports

Figure 2: European Active Manager Underperformance by Region

Source: S&P Dow Jones

Past performance: A clever marketing trap that keeps on catching

Checking past performance is a good way to sieve out winning funds, right? Wrong again!

Somewhat surprisingly, it turns out that past performance is a poor tool to separate the wheat

from the chaff.

Worse, it’s a marketing trap and it works like this:

By the law of averages, some funds will always outperform their benchmark in any period. The

question is whether these funds are likely to keep on outperforming, or whether they were just

lucky? To answer this, financial statisticians search for what is known as ‘positive serial

correlation’, a mathematical indication of whether a fund possesses a true durable edge.

It turns out that positive serial correlation is about as elusive as the Tibetan Yeti!

It gets worse!

Where performance persistency can be identified, it is persistently poor performance. In other

words, the cohort of active funds which outperforms in one period, show little propensity to keep

on outperforming in the future. Whereas losing funds show a propensity to keep on losing.

Full report from the UK’s Financial Conduct Authority (FCA) here:

https://www.fca.org.uk/publication/market-studies/ms15-2-3.pdf

Fund management houses can count themselves lucky that such mathematical analysis is

beyond the capability of most retail investors. According to the “OECD Financial Literacy and

Inclusion Report 2013”, 61% of U.K. participants were able to respond correctly to a simple

question on the calculation of interest plus principal, whereas only 37% were able to correctly

identify the effect of compound interest.

By extension, very few people understand positive serial correlation. As a consequence,

active fund managers are free to showcase funds which happen to have outperformed in a given

period, knowing full-well that retail investors using simplistic 3-, and 5-year performance data will

walk right into their cunning trap.

Is this legal? Of course, it is. The ubiquitous disclaimer is stark enough, "Past performance is no

guarantee of future results". The trouble is, most of us forget that this yada-yada warning is deadly

serious.

Active fund marketing departments have still more arrows in their quiver. They can, for example,

attract interest in underperforming funds by conjuring-up gambling instincts. That is the incorrect

belief, that if a particular event occurs more frequently than normal during the past, it is less

likely to happen in the future.

Alas, all roads lead to Rome for the unsuspecting retail investor. Whether he/she buys a fund that

has recently out– or underperformed, spending one’s life riding ‘downward escalators’ is a recipe

for serial wealth destruction. While gains may be made in absolute terms, the level of

performance will be far behind raw stock market returns.

Why do so many active funds claim to outperform?

Most active funds choose to measure themselves against their peers, not their relevant

benchmark index. If their peer group perform badly on average – and we have just seen they do

– then a fund that is performing better than its peers will end up near the top of a bad bunch.

And so it goes; fund managers give their finest rendition of “Always Look on the Bright Side of

Life”, while beleaguered savers yearn after benchmark index returns, by now a distant dot on the

horizon.

Others fund managers measure themselves against composite benchmarks that blend equity,

bond, and other indices in a proportion that broadly represents the fund’s long-term asset

allocation. This has advantages, although fund management houses inevitably choose

benchmarks designed to flatter.

Another related problem is third-party ratings (3*, 4*, 5* rated funds, etc.), Best Buy lists, and

Financial Awards, which retail investors rely heavily upon when choosing a fund.

Firstly, few are aware that these awards are, in effect, often paid for by the funds themselves.

Secondly, the FCA tells us that the returns of these funds over their chosen benchmark is

indistinguishable from zero, and that they do not outperform net of charges.

Poor risk-adjusted returns and ‘closet indexing’

Investment is all about balancing risk and reward and we should not criticise an active manager

for underperforming an index if he/she is shown to be taking less risk than their relevant index.

Once again, in 2021 S&P Dow Jones dashed this explanation:

“For the three-year period, 70% of Europe Equity funds had worse risk-adjusted returns than the

S&P Europe 350. Over the 10-year period, this figure rose to 87%.

Which gives birth to yet another problem, ‘closet indexing’: Poorly performing funds are naturally

incentivised to de-risk and seek the anonymity of the herd. Enter ‘closet indexing’, a practice

whereby a fund manager holds themselves, and charges, as if they were an active fund, while in

practice simply tracking the benchmark index.

According to the European Markets Regulatory Authority, ESMA, up to 15% of European funds are

misleading investors into believing that they are exposed to a different set of risks and returns to

the ones they are getting.

In 2017, the FCA found that £109 billion of UK active funds closely mirrored the market, despite

being significantly more expensive than their passive comparators.

A short but good life …for the fund houses!

In the end, Feynman’s ‘reality’ prevails at great cost to the retail investor. According to S&P Dow

Jones:

“Over 20 years, nearly 70% of domestic equity funds and two-thirds of internationally focused equity

funds across segments were confined to the history books.”

Some funds are quietly ‘disappeared’, while others are folded into better performing funds,

making it difficult for retail savers to reconcile the returns of their portfolio.

Nevertheless, with few regulatory obligations to produce performance data beyond 5-years,

glossy marketing prowess can normally ensure a decent and profitable life for these funds. That

is, from the perspective of the fund managers and executives who have expensive lifestyles and

their own retirements to support.

The marketing endgame works like this:

Despite some 95% of active funds underperforming over a 10-year horizon, active fund managers

love to regale their investors about the long-term durability of their market expertise. While

claims of “evergreen” investment strategies often border on fraudulent, fund houses routinely

claim their funds have simply hit a bad patch.

The reality is that many active funds have simply been rendered obsolete: Because unlike

physical sciences, where the rules remain largely static, finance is an ever-changing kaleidoscope

of new technology, evolving human behaviour, and changing geopolitical systems.

How is this legal? For the simple reason that nobody has a crystal ball to prove in advance that a

fund has not found the Holy Grail. The curtain will only fall when a fund is ultimately found out.

Not the final curtain of course, a few refreshing interval drinks and up the curtain rises on Act II: a

new attractively named fund such as the “The Enhanced Leveraged Alpha Fund”.

On the process goes with Acts III, IV, V, VI, etc.

It works for the fund houses, not for you. In 2016, the FCA noted that the operating margins of UK

asset managers were 34–39% compared to an average operating margin of 16% for the other

industries in the FTSE All Share Index.

Active funds can still play an important role in retail portfolios

There are many good active funds around which can play a useful role in retail portfolio

investment, diversification, and risk mitigation.

Even if we don’t want to hold these funds forever, tactical opportunities can arise. For example,

when a fund’s constituents are hammered by poorly judged selling pressure, or when a

specialised fund is difficult recreate. Or simply when one rates a talented fund manager during a

particular phase of the business cycle.

But be aware: while many attractive funds exist, professional investors negotiate hard and

effectively to ensure they get good value for money. They typically pay much lower fees than

retail investors to invest in the same funds.

Conclusion

The data is clear, a portfolio of professionally managed active funds is almost certain to

significantly underperform its relevant stock and bond indices over the longer term.

This may seem harsh, but there it is; a reality that cannot be fooled by glossy marketing and

selective truths.

For those interested, we will shortly publish on our website an examination into the root causes

of why active funds underperform in the manner we have just seen.

In Part 2 of this series, we will explore the murky world of fees, and in Part 3 we are excited to

share with you techniques we have developed to overcome the problem.

Andrea Badelt, Partner

The Hidden Underperformance of Active Funds

Behind the Curtains of the Assert Management Industry #1

| 23 June 2021

BY ANDREA BADELT, PARTNER

Eriswell Market Insights

+44 (0) 1932 240 121

info@eriswell.com

© 2024 Eriswell Capital Management LLP